3 Stocks I'm Buying Now (February 2024)

Up Next

8 videos

Should you buy Rocket Lab stock? (April 2024)

April 8th, 2024

Should you buy ResMed stock? (February 2024)

February 21st, 2024

Should you buy Boeing stock? (January 2024)

January 16th, 2024

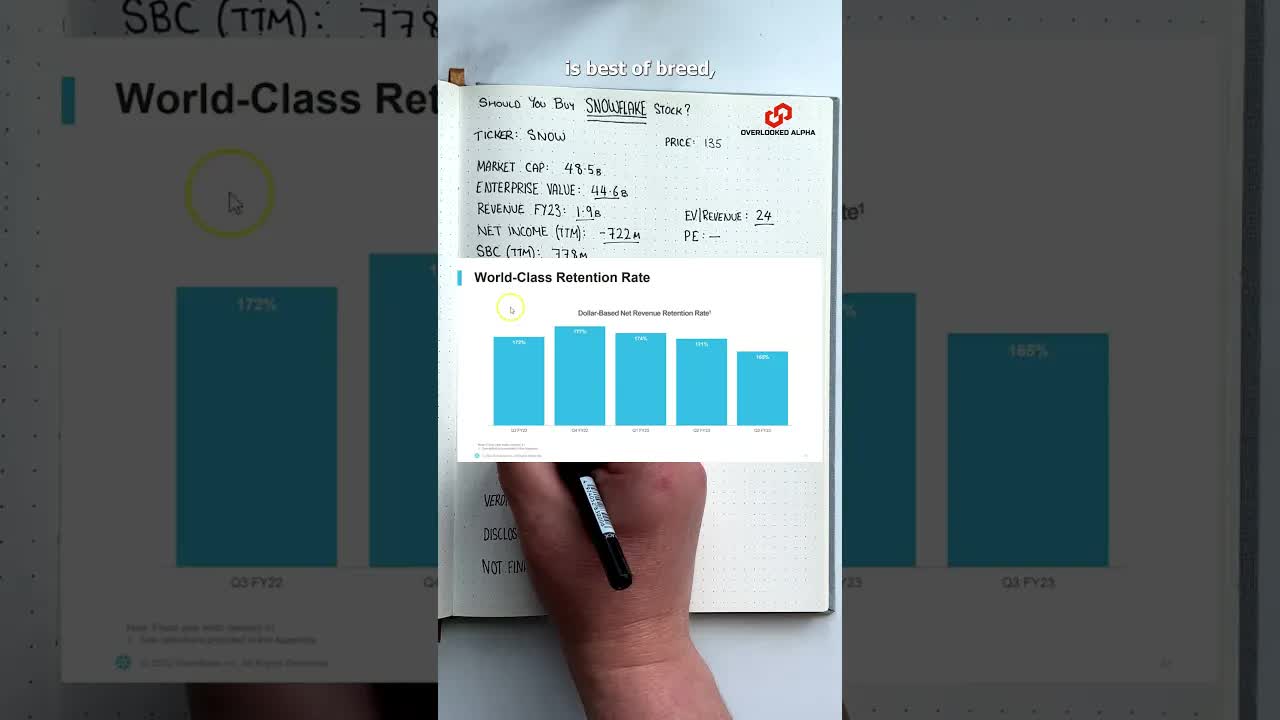

Snowflake stock analysis #shorts

December 1st, 2022

3 Stocks To Avoid November 2024

November 19th, 2024

PayPal Stock Is In A Tight Spot - 3 Minute Stock Analysis - May 2025

May 25th, 2025

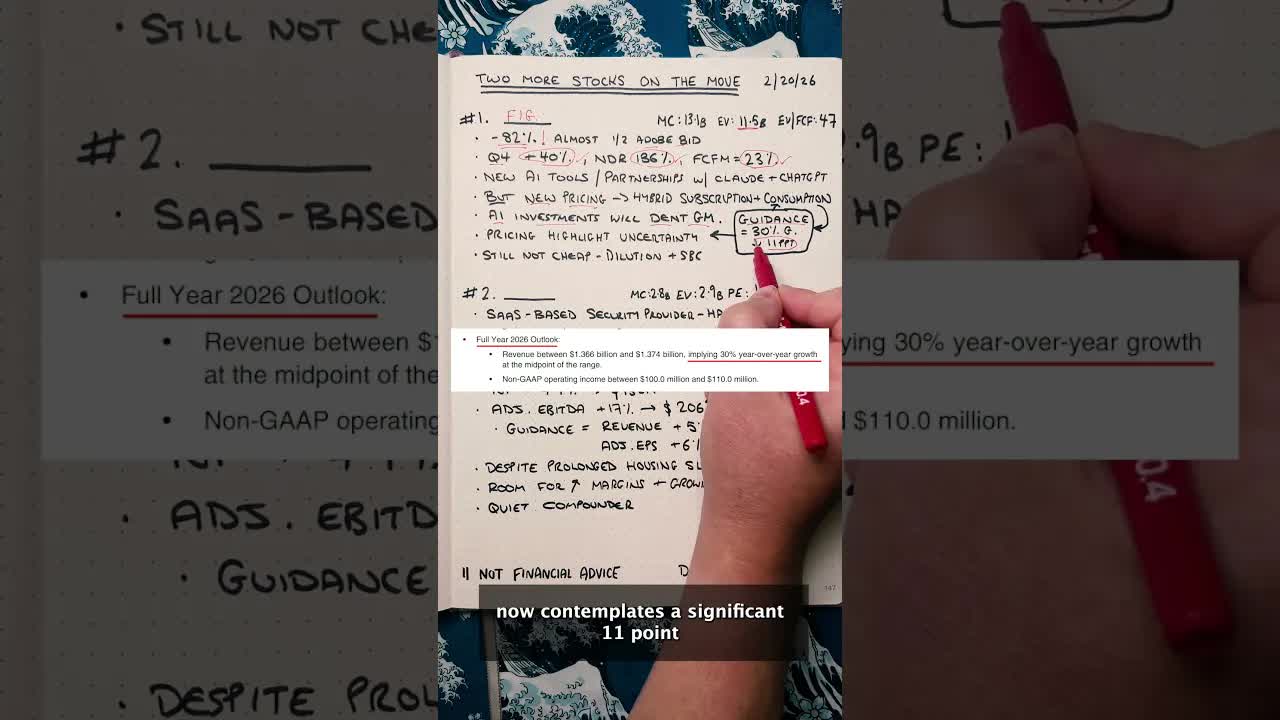

Two Stocks That Moved This Week #stocks #economy #stockanalysis

February 21st, 2026

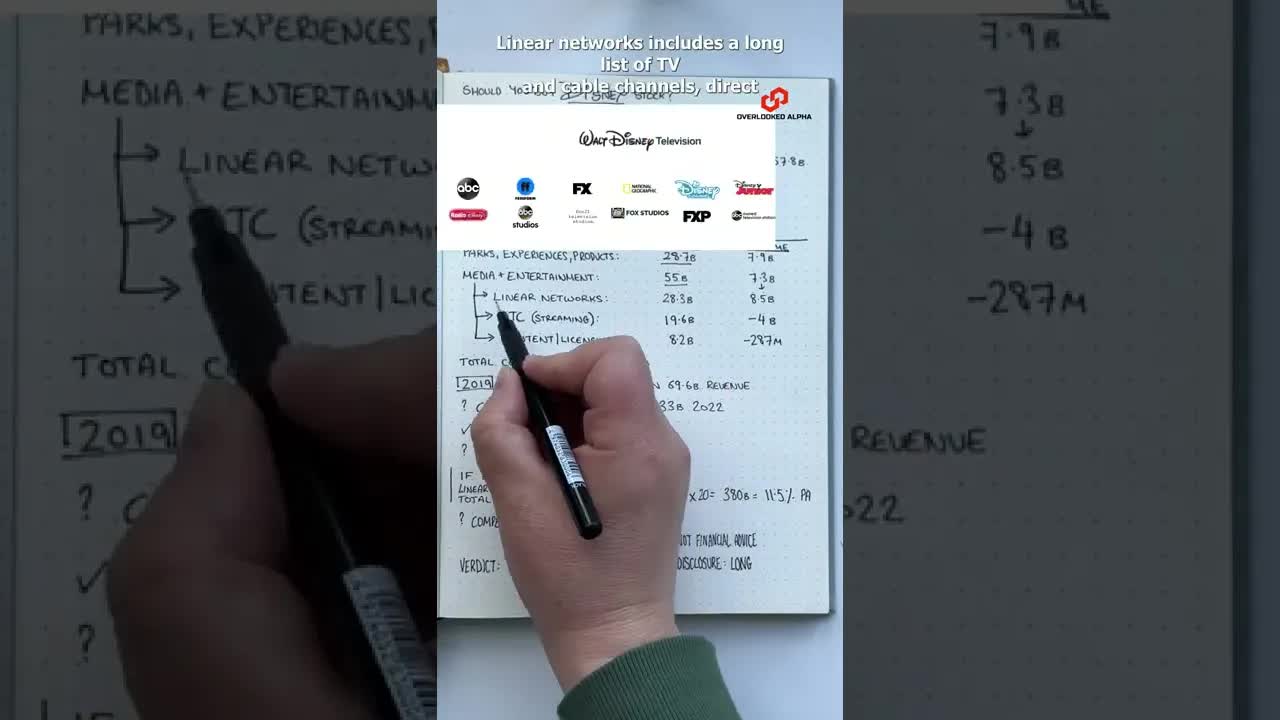

How does Disney make money? #shorts

November 19th, 2022

Published first at https://www.3minutebreakdowns.com 3 stocks I like February 2024. Tickers: $ULTA $TSM $PLTR Number one. Ulta Beauty. MC: 24.6 billion Ulta is the largest beauty retailer in the US. It’s got around 1400 stores and the market cap is just under 25 billion dollars. With 1.2 billion of net income over the last 12 months the stock is valued at about 21 times earnings which is much lower than the historical average. Back in 2017 the PE ratio was above 40. What I like most about Ulta is the company's financial discipline. The company has a history of strong profitability, increasing profit margins and share buybacks that have reduced the share count by almost a quarter. And even during the pandemic, when Ulta had to shut many of its stores, the company still managed to make a profit. Ulta has a growing loyalty program and I think more growth can come from the pop up stores that it’s started doing with retailer Target. But just a modest amount of growth should be enou gh to send the stock higher. Number Two, TSMC. MC: 618 billion TSMC is the world’s largest manufacturer of microchips supplying tech companies like Apple, Nvidia, AMD and many more. It’s no secret that microchips are in huge demand and that demand will only increase with megatrends like AI and electric vehicles. And as the world’s leading manufacturer TSMC has significant pricing power. This can be seen in the company’s strong net income margins of 39%. TSMC’s latest earnings report was also solid. The company revealed increasing uptake for its most advanced 3 nanometre chip. The company also said revenue growth in 2024 should climb above 20%. That takes the forward PE ratio below 20 which seems more than reasonable. Number Three, Palantir. MC: 51.7b Palantir reported earnings this week causing the stock to jump 30%, taking the market cap above 50 billion dollars. At first glance, the stock now looks incredibly expensive at 23 times revenue and 246 times earnings. But the key point with Palantir is that growth seems to be accelerating. US commercial revenue grew 70% in the fourth quarter thanks to demand for its AIP software. And Palantir bootcamps seem to be doing a great job of selling the product. Equally impressive, Palantir’s adjusted free cash flow margin more than doubled to 50%. These kinds of metrics mean that Palantir deserves a high multiple. And although the stock looks expensive, momentum should keep the shares moving higher. #stockstobuy #stocks #investing