Should you buy Amazon stock? (August 2023)

Up Next

8 videos

Should you buy Cloudflare stock? (May 2024)

May 6th, 2024

Should you buy First Solar stock? (February 2024)

January 31st, 2024

Palantir Stock Analysis (January 2024)

January 15th, 2024

Should you buy Lucid stock? (July 2023)

July 6th, 2023

3 Stocks I'm Buying Now (June 2024 Edition)

June 6th, 2024

Should you buy PayPal stock? (August 2024)

August 5th, 2024

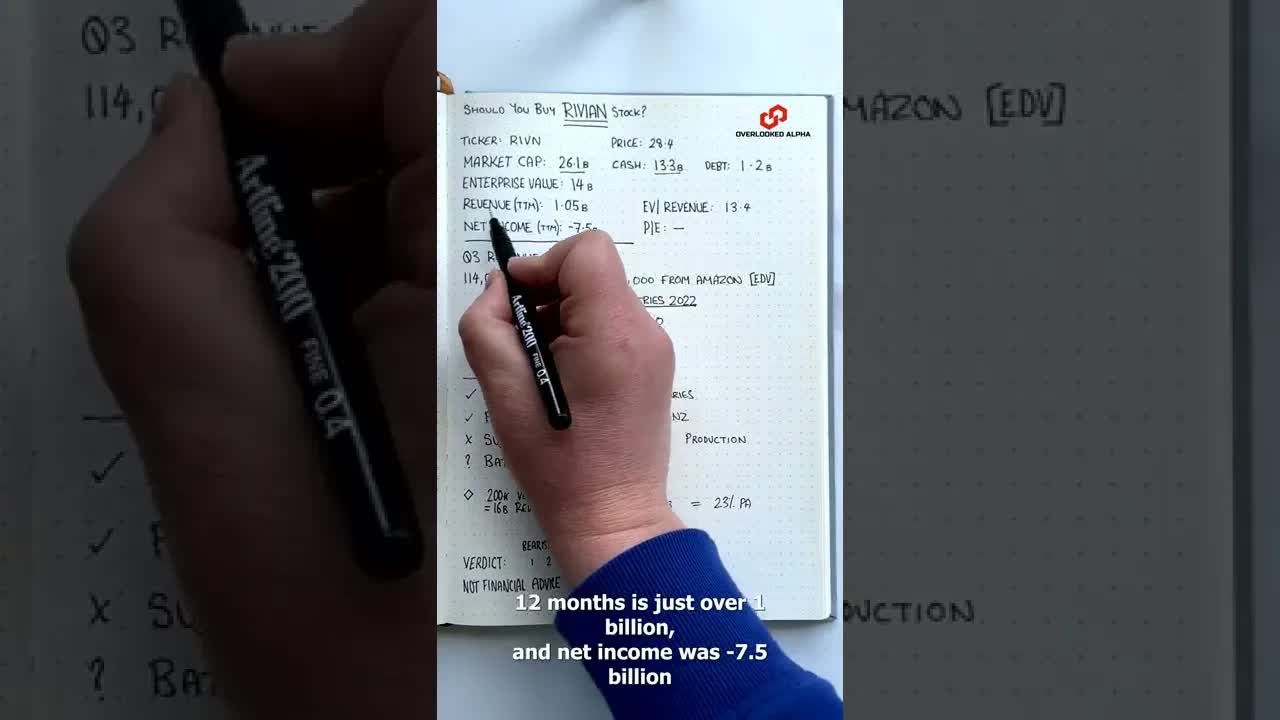

Rivian stock analysis #shorts

November 25th, 2022

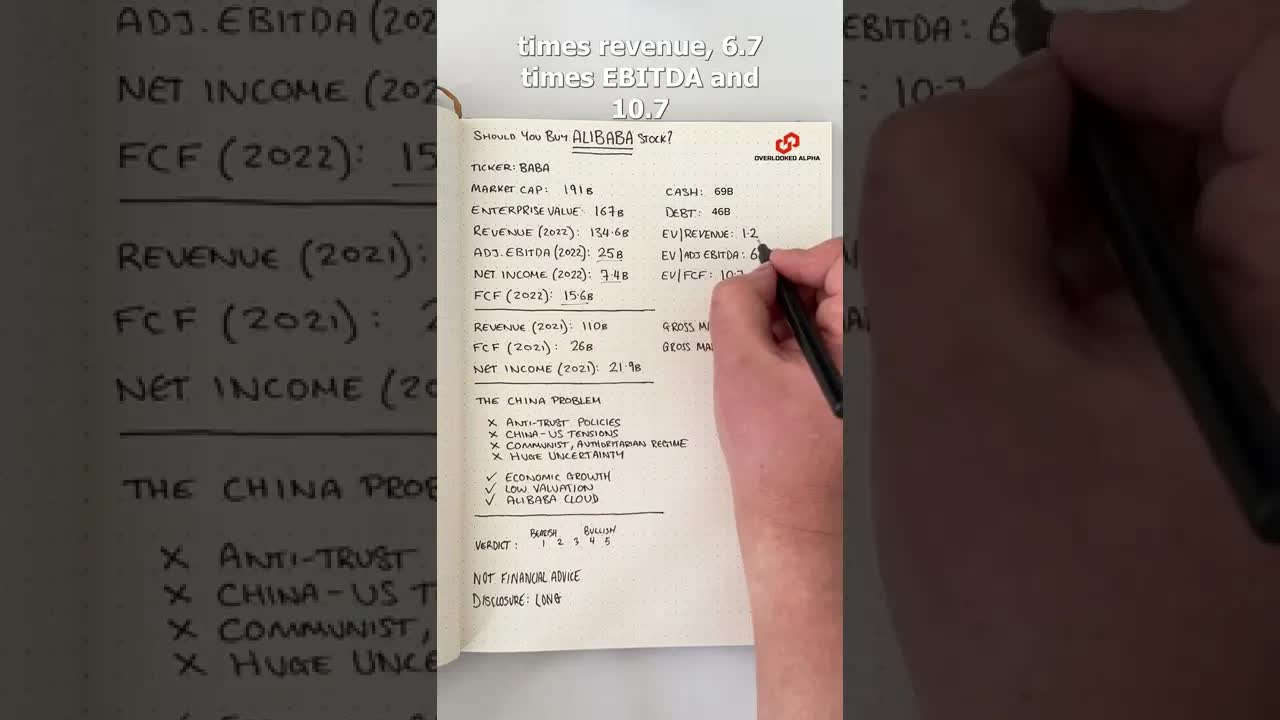

Should you buy Alibaba stock? #shorts

October 25th, 2022

Amazon stock analysis. Ticker: AMZN. Join 9000+ investors: https://www.overlookedalpha.com Amazon stock is up 65% this year taking shares up to $138. At that price the company has a market cap of 1.42 trillion. The balance sheet has 54 billion of cash and 18 billion of investments as well as 67 billion of debt so the enterprise value is also 1.42 trillion. Revenue over the last 12 months is 538 billion, with 13.1 billion of net income, 63 billion of adjusted ebitda and 3.2 billion of free cash flow. So Amazon stock is valued at 2.6 times revenue, 22 times ebitda and 101 times earnings. Valuing the stock based on these company-wide metrics isn’t that useful, however, for two reasons. First, Amazon continues to reinvest its profits back into the business and that skews its price to earnings ratio. Second, Amazon is made up of several different businesses and each one has different profit margins and growth rates. It’s online stores segment includes product sales such as books, videos, games, music and software. This segment contributes the most amount of revenue, 222 billion over the last 12 months but it’s also the least profitable and it grew only 4% in the latest quarter. It’s third-party seller service includes product and fulfilment fees and contributes 127 billion of revenue at a growth rate of 18% year over year. We don’t know precisely what the profit margins are but 3rd party services is clearly a strong business. Unit volume was up 60% over the quarter and Amazon fulfillment has been taking share from traditional carriers like Fedex and UPS. Amazon Web services provides on-demand cloud computing and is Amazon’s most profitable segment with operating margins of 24% in the latest quarter. This segment grew 12% to 85 billion of annual revenue. #amznstock #stockstobuy #investing #overlookedalpha