Should you buy Twilio stock? (June 2024)

Up Next

8 videos

Should you buy C3.ai stock? (AI stock analysis)

June 19th, 2023

Should you buy Cava stock? (April 2024)

April 23rd, 2024

Should you buy Dutch Bros stock? (April 2024)

April 6th, 2024

Should you buy Uber stock? (November 2023)

November 10th, 2023

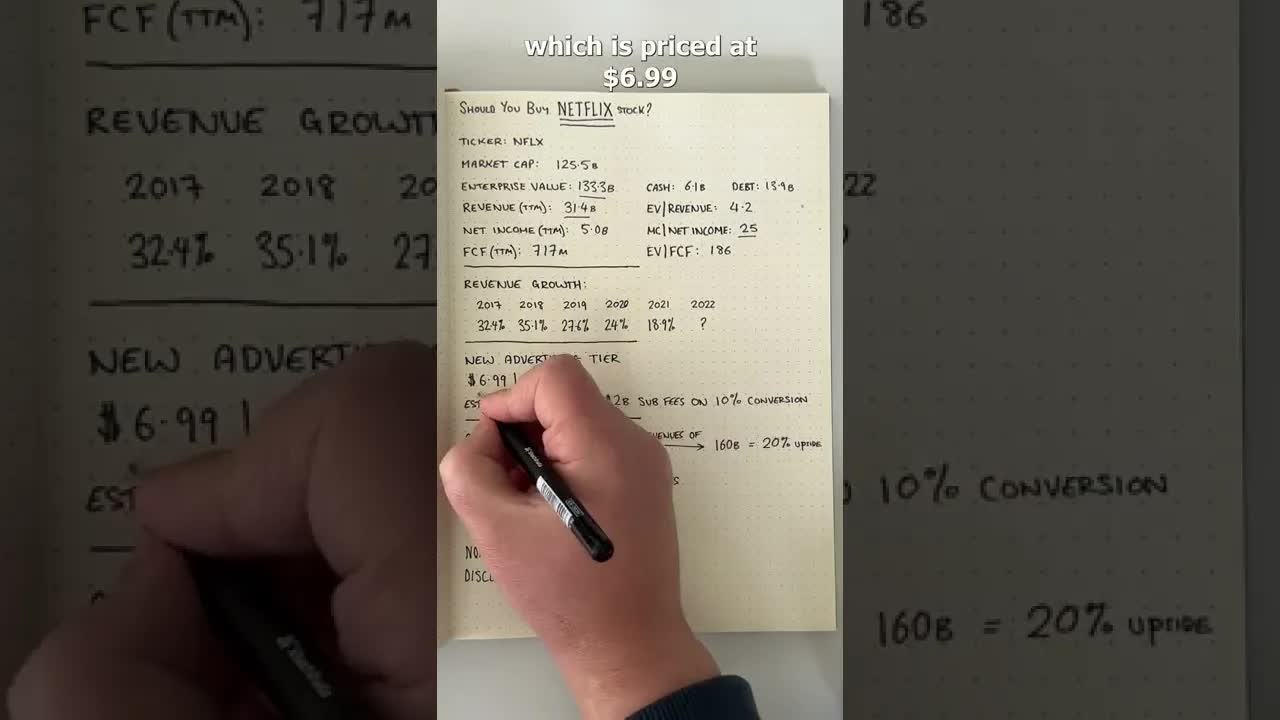

Is Netflix stock a buy? #shorts

October 25th, 2022

Should You Buy Google Stock? #Shorts

October 11th, 2022

Should you buy Nvidia stock? (November 2024)

November 21st, 2024

3 Cheap Stocks! (March 2025)

March 5th, 2025

Published first at https://www.3minutebreakdowns.com Twilio stock analysis. Ticker: $TWLO Twilio provides APIs that developers use to embed messaging applications like SMS, email and push notifications. These applications allow companies to communicate and engage with customers. Twilio stock soared during the pandemic but has since come back to earth. At the current price, the company has a market cap of 10.6 billion dollars. With 4.4 billion of cash and investments and just under 1 billion of debt the enterprise value is 7.2 billion. Revenue over the last 12 months comes to 4.2 billion with 660 million of adjusted ebitda and 655 million of free cash flow. But the company is not GAAP profitable. Net income over the last 12 months is negative 729 million owing to high marketing costs and high levels of stock based compensation. To be fair, Twilio has taken steps to address stock-based compensation. The company has slashed its workforce by 33% and implemented a buyback scheme that, if completed, should reduce the outstanding share count by 20%. The company has also cut operating costs and invested in a new product called Segment which uses customer data to help companies personalize their services. So Twilio has made an effort to streamline its business. And at 11 times free cash flow the stock can provide strong upside if the company can now get growth back on track. Revenue growth at Twilio, however, looks underwhelming. Sales grew less than 9% last year and on a trailing twelve month basis growth is only 6%. Management doesn’t expect a huge improvement in the rest of this year either. Also worrying is the company’s net expansion rate which has been trending down consistently over the last few years, hitting 102% in the latest quarter. #stocks #investing #stockanalysis #3mb