Should you buy Zoom stock? (July 2023)

Up Next

8 videos

Should you buy Meta stock? (February 2024)

February 2nd, 2024

SoFi Stock Analysis (December 2023)

December 2nd, 2023

Should you buy Rolls Royce stock?

May 28th, 2023

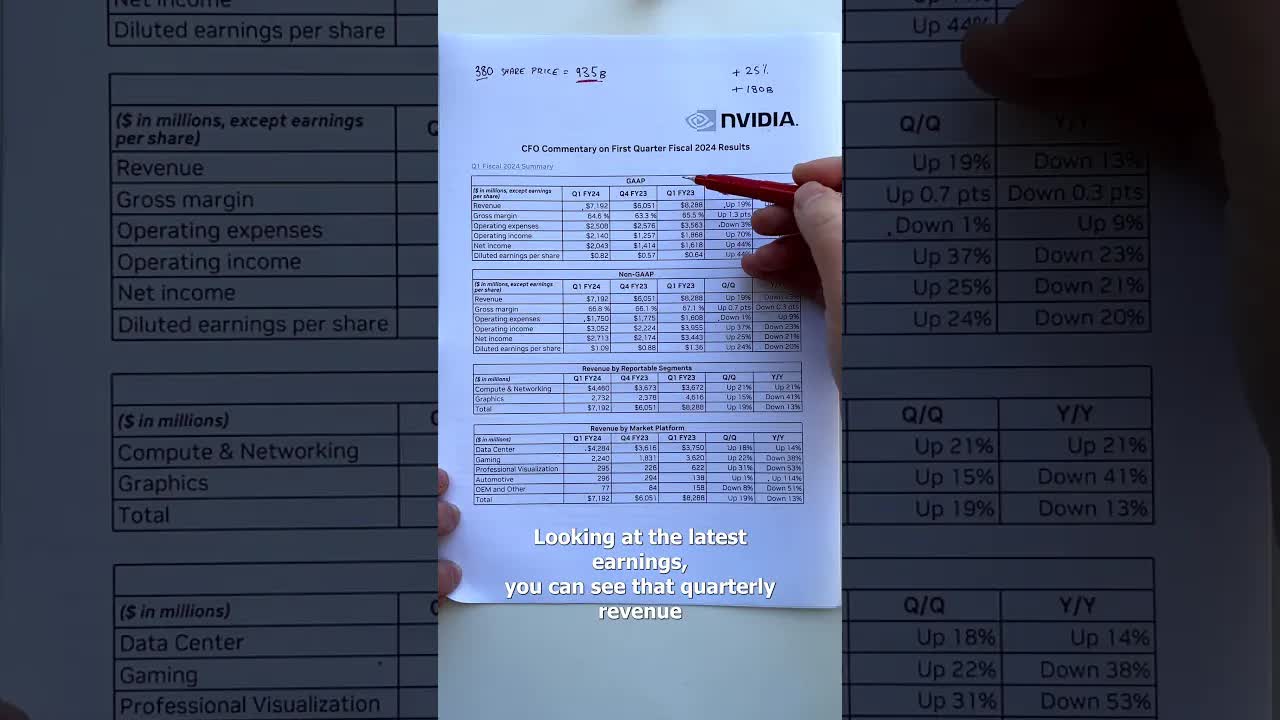

Nvidia Stock Update (Part 1) #shorts

May 25th, 2023

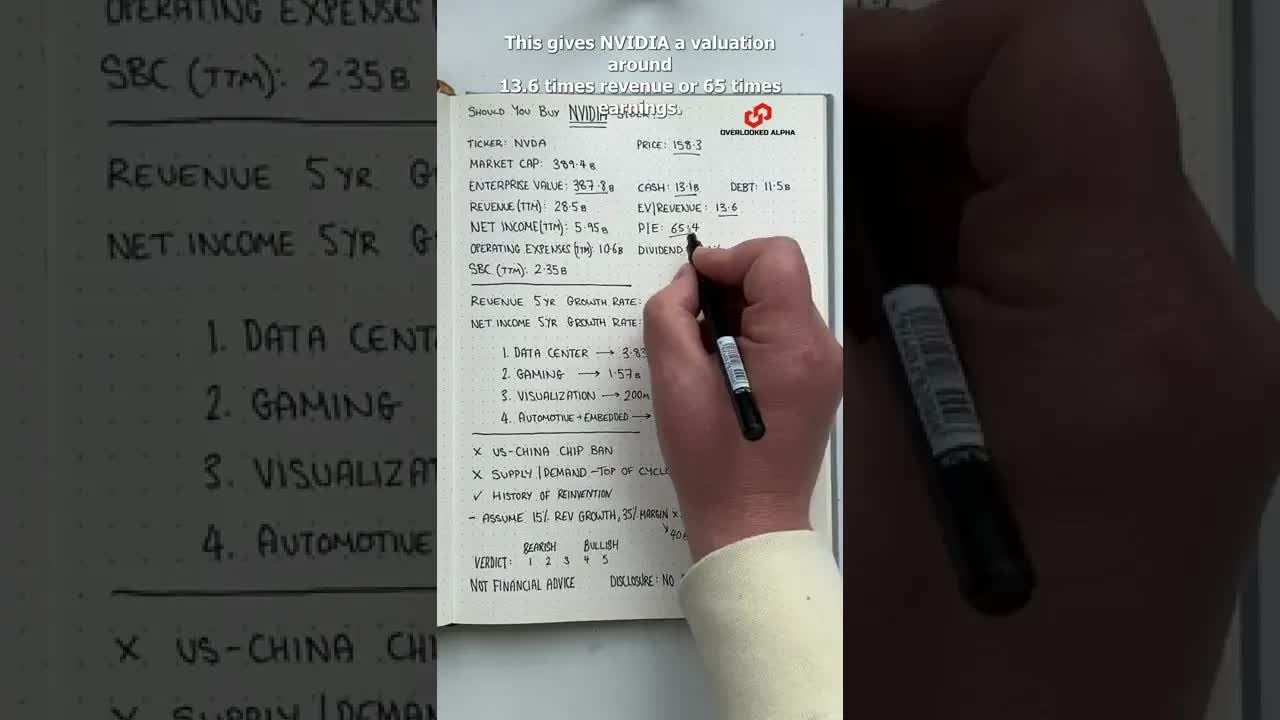

Nvidia stock analysis #shorts

November 29th, 2022

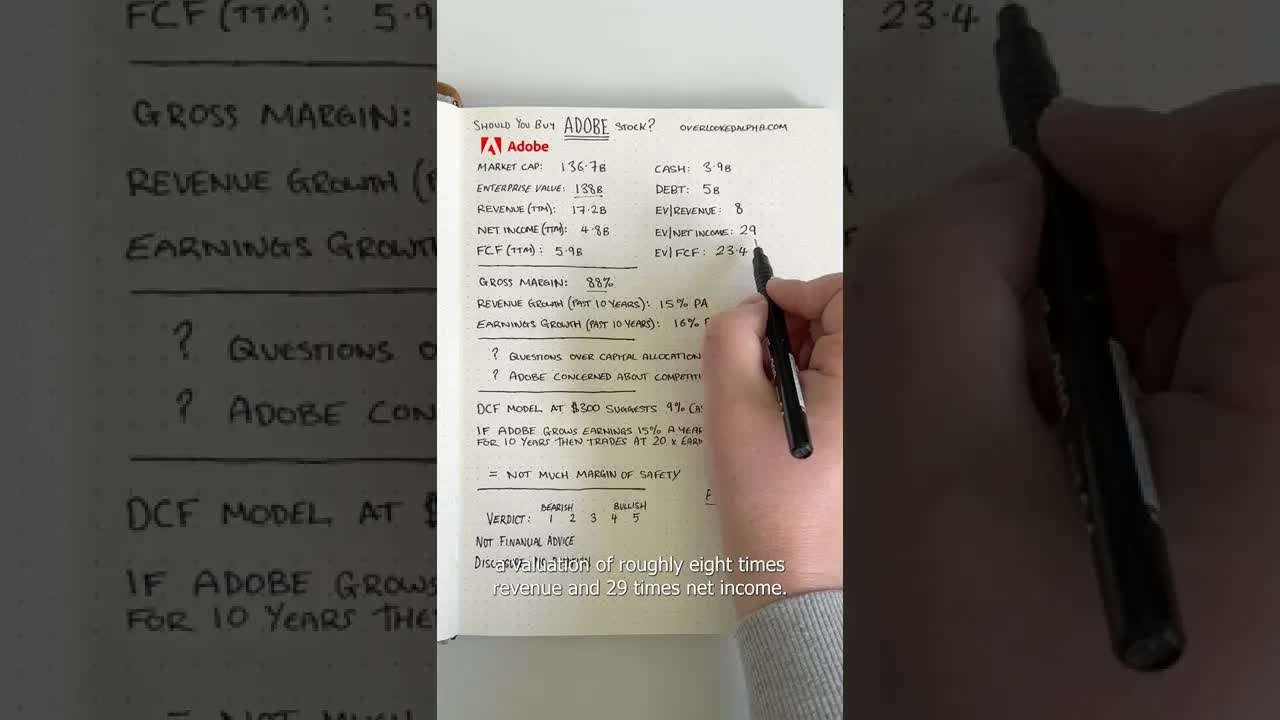

Should you buy Adobe stock? #shorts

October 18th, 2022

3 Stocks To Buy In A Market Crash (April 20250

April 9th, 2025

Google Stock is Looking Cheap - 3 Minute Stock Analysis - May 2025

May 6th, 2025

Zoom stock analysis. ZM stock. Give us a try: https://www.overlookedalpha.com Zoom Video was one of the biggest beneficiaries of the pandemic. Between 2020 and 2021, revenue grew over 300% and the stock soared more than 600% taking the market cap to 160 billion. Since then, however, revenue growth has slowed to single digits and the stock price has come back to earth. Today, the company has a valuation just over 20 billion. With 6 billion of cash and investments, and zero debt, the enterprise value is roughly 14 billion. Revenue for the rest of the year is expected to come in at 4.47 billion which represents less than 2% annual growth. Free cash flow looks good at just over a billion but net income has collapsed from a peak of 1.4 billion in 2022 to just 5.5 million over the last 12 months. That means Zoom stock is now valued at 3.2 times revenue, 13 times free cash flow and over 4000 times earnings. So why is the company reporting such a huge drop in net income? A major reason is stock based compensation which totals almost 1.4 billion over the last 12 months. That figure is now 30% of revenue. A second reason is that the company has seen a significant increase in operating expenses. Looking at the table you can see that R&D makes up 19% of revenue and G&A is 15% of revenue. Nothing strange there, but what is strange is that Zoom is spending 1.8 billion dollars on sales and marketing (40% of revenue) and it’s only achieving modest growth. In fact, sales and marketing spend was up 55% in the first quarter while revenue increased only 3%. This suggests Zoom is spending a lot of money to keep existing customers on the platform and it’s a worrying sign when combined with the growth outlook. #zoomstock #stocks #stockstowatch #investing