Should you buy Rolls Royce stock?

Up Next

8 videos

Celsius Stock Analysis (November 2023)

November 19th, 2023

Should you buy Chewy stock? (September 2023)

September 26th, 2023

Should you buy Marvell Technology stock?

June 7th, 2023

Should you buy Xpel stock? (June 2024)

June 3rd, 2024

Should you buy Rivian stock? (July 2024)

July 7th, 2024

Should you buy Adyen stock? (August 2024)

August 27th, 2024

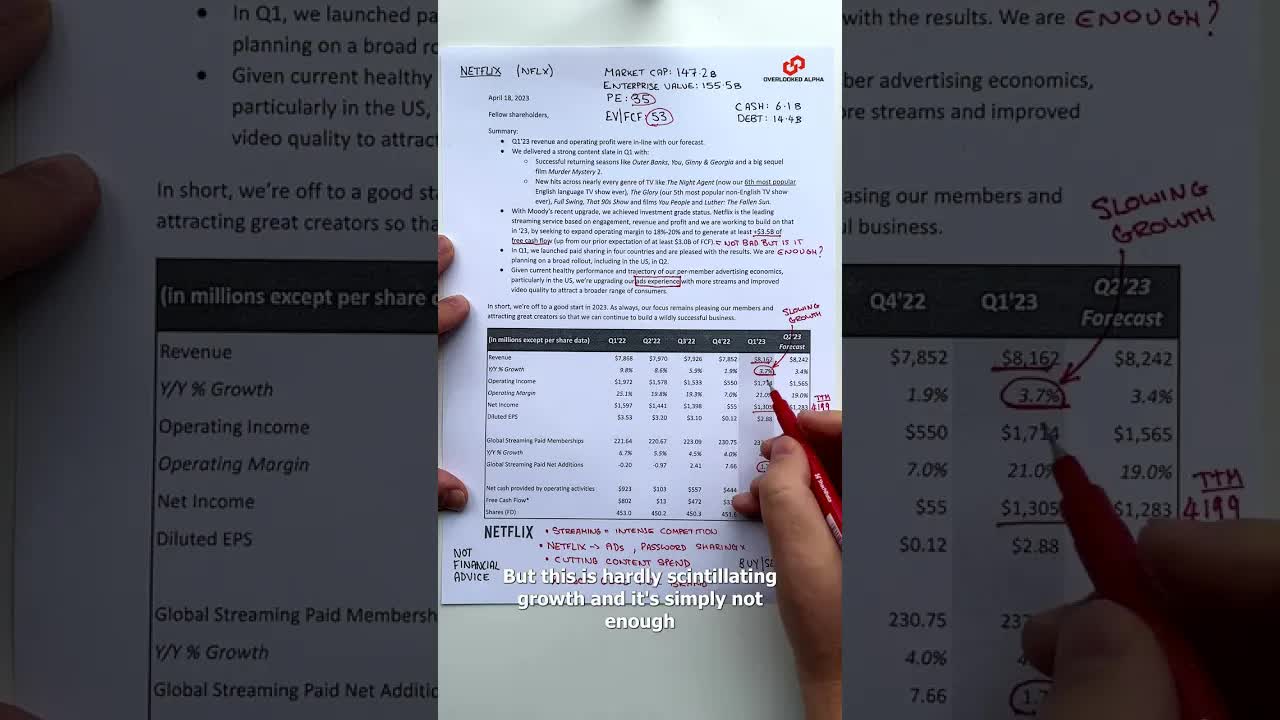

Netflix earnings wasn't too hot #shorts

April 21st, 2023

How to follow famous investors (free tool) #shorts

April 26th, 2023

(Only just realized YouTube accepts vertical videos 🤦♂️) Rolls Royce stock analysis. RR.L stock. Join the newsletter: https://www.overlookedalpha.com When someone mentions “Rolls-Royce” the first thing that springs to mind is the brand of British luxury cars. However, Rolls-Royce Holdings, the public company that trades on the London Stock Exchange, is predominantly an aerospace and defense company. It’s the world’s second-largest manufacturer of aircraft engines, after General Electric. And it operates across 4 key segments. Civil Aerospace- this includes the development and production of commercial aircraft. Defense includes the development of military aircraft and nuclear submarines. Power systems including on-site power and propulsion systems. And New markets which includes the manufacture of small modular reactors and new electric power solutions. Currently, civil aerospace contributes 45% to the company’s total revenue, defense is 29% and power systems is 26%. The new markets segment is currently small and doesn’t produce much revenue at all. The defense sector is the most profitable one, accounting for 60% of the operating profit, followed by power systems for the remaining 40%. Civil aerospace, the largest segment by revenue, contributes only 20% of profit. Currently, Rolls Royce has a market cap of 13.1 billion pounds. With 3.1 billion of cash and investments and 5.6 billion of debt, the enterprise value is 15.6 billion. From an operating point of view, the company looks healthy with £900m in operating profit. The trouble is what lies below that line in the income statement. Taking into account £12b in contract liabilities Rolls Royce net financing cost for 2022 was a staggering £2.4 billion. This is not a fair representation, because £1.9b was related to losses on foreign currency contracts. Still, even after the adjustment, significant debt obligations put the company at risk. And so we have negative net income to the tune of 1.2 billion and low gross margins of 20%. Reducing the level of debt has to be the #1 priority of the management, especially in an environment where the interest rates are rising. Rolls-Royce operates in a very complex environment, and its financials aren’t simple either. This doesn’t give a lot of confidence in the eyes of the investors, so the share price decline of almost 50% in the last 5 years doesn’t come as a surprise. #stocks #investing #stockmarket #stockstowatch