Should you buy Laurent Perrier stock? (October 2024)

Up Next

8 videos

Adyen Stock Analysis (September 2023)

September 19th, 2023

Should you buy Rocket Lab stock?

June 21st, 2023

Should you buy UiPath stock? (June 2024)

June 21st, 2024

Nvidia Stock Update (Part 2) #shorts

May 25th, 2023

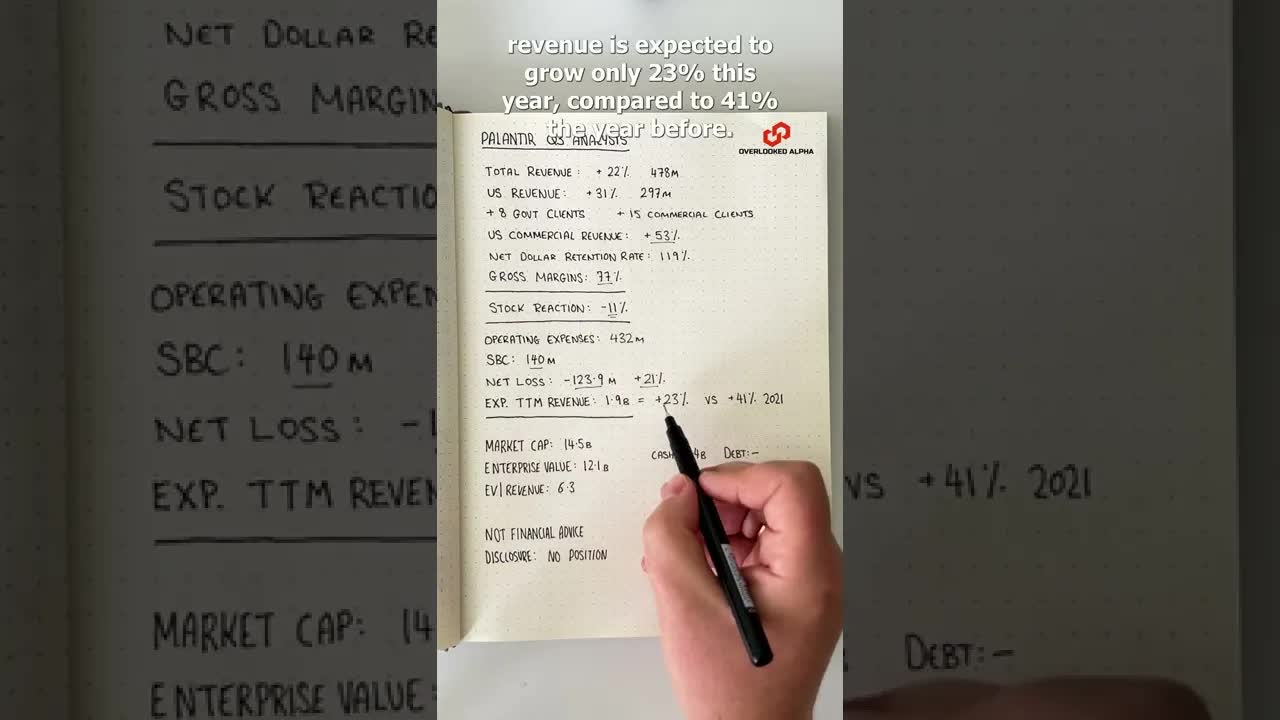

Palantir Stock Q3 Update #shorts

November 8th, 2022

Should you buy SoundHound AI stock? (December 2024)

December 10th, 2024

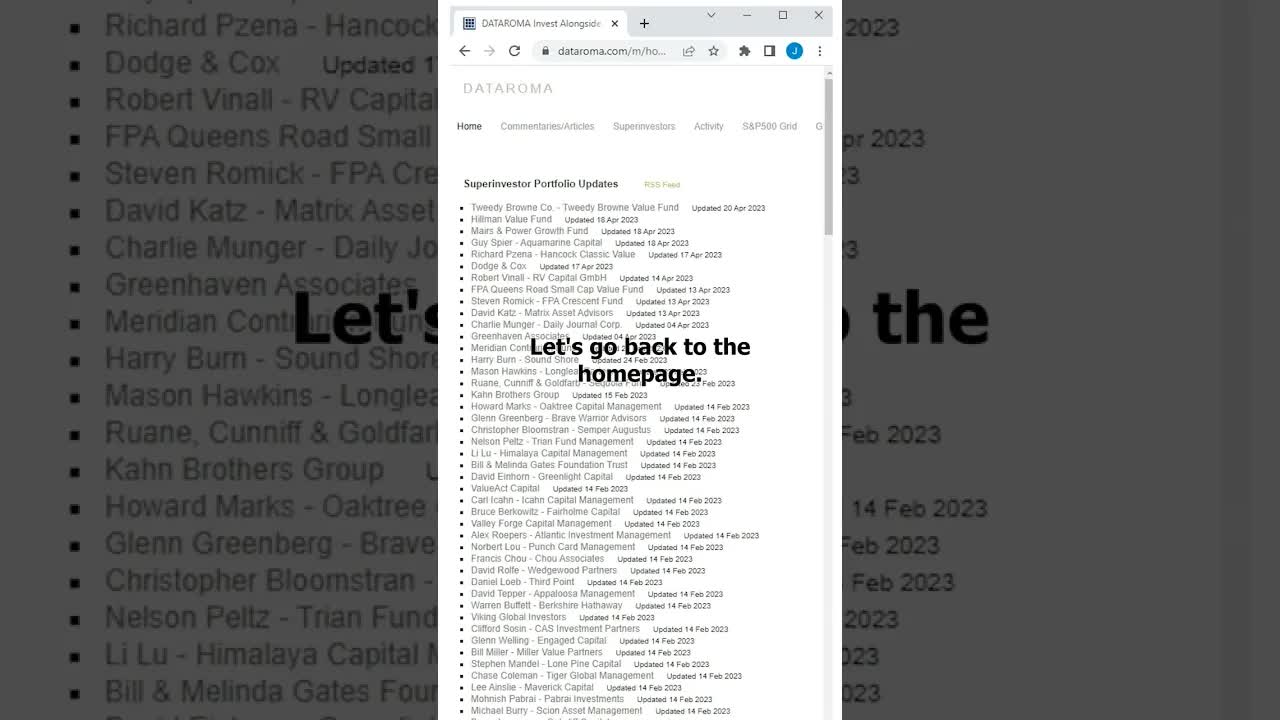

How to follow famous investors (free tool) #shorts

April 26th, 2023

Where to get data for company analysis #shorts

January 23rd, 2023

Published first at https://www.3minutebreakdowns.com Laurent Perrier stock analysis. Ticker: $LPE.PA Laurent-Perrier makes some of the world’s most exclusive champagne but shares have fallen 17% this year taking the company’s market value to 590 million euros. With 183 million of net debt the enterprise value is 773 million. Revenue over the last 12 months comes to 313 million euros with 64 million of net income and 100 million of ebitda. So Laurent Perrier stock is valued at just 9 times earnings and under 8 times EBITDA. That valuation is lower than the stock received during the 2008 financial crisis. Price to tangible book value (which accounts for Laurent Perrier’s vast Champagne stores) also looks cheap at the bottom of the historical range. Meanwhile, Laurent Perrier has been performing well in a difficult market. Global champagne sales fell 8.2% last year but Laurent Perrier’s profits increased 8% thanks to higher pricing. As a result, Laurent Perrier’s margins have soared to record levels with gross margins hitting 61% and operating margins 30%. So why is the stock so cheap? There are several issues to be aware of. The first is that Laurent Perrier’s record margins are unlikely to be sustainable. Champagne typically takes 4 years to develop, so it’s possible that the company’s margins are yet to incorporate the effects of higher inflation. Reported costs could soon go up which means margins should decline going forward. After all, the champagne industry is centuries old and it seems unlikely that Laurent Perrier has found a clever new way to extract significantly higher profits. #investing #stocks #champagne #stockstowatch